Onchain yield has a correlation problem

April 28, 2026

Onchain yield has a correlation problem

Scroll through the curators on any major DeFi lending protocol and you'll find dozens of vaults allocating essentially the same underlying assets or markets.

The implications are underappreciated – particularly as institutional capital begins flowing into onchain yield products and expects the same portfolio construction discipline it applies everywhere else.

CoinShares – the only asset manager currently regulated under AIFMD, MiFID, and MiCA – recently published detailed factsheets on their onchain yield strategies built with Railnet. The data makes the correlation problem concrete, and their approach to solving it reveals something important about where onchain infrastructure falls short.

The single-factor problem

The entire discipline of institutional fixed income is built on a foundational insight: combining uncorrelated return streams produces better risk-adjusted outcomes than concentrating in any single one. Multi-strategy credit funds, macro-relative-value portfolios, diversified income mandates – all variations on the same principle.

The majority of USDC vault strategies allocate almost exclusively across DeFi lending protocols that share the same supply-demand dynamics. When utilisation drops across onchain lending markets, it drops everywhere.

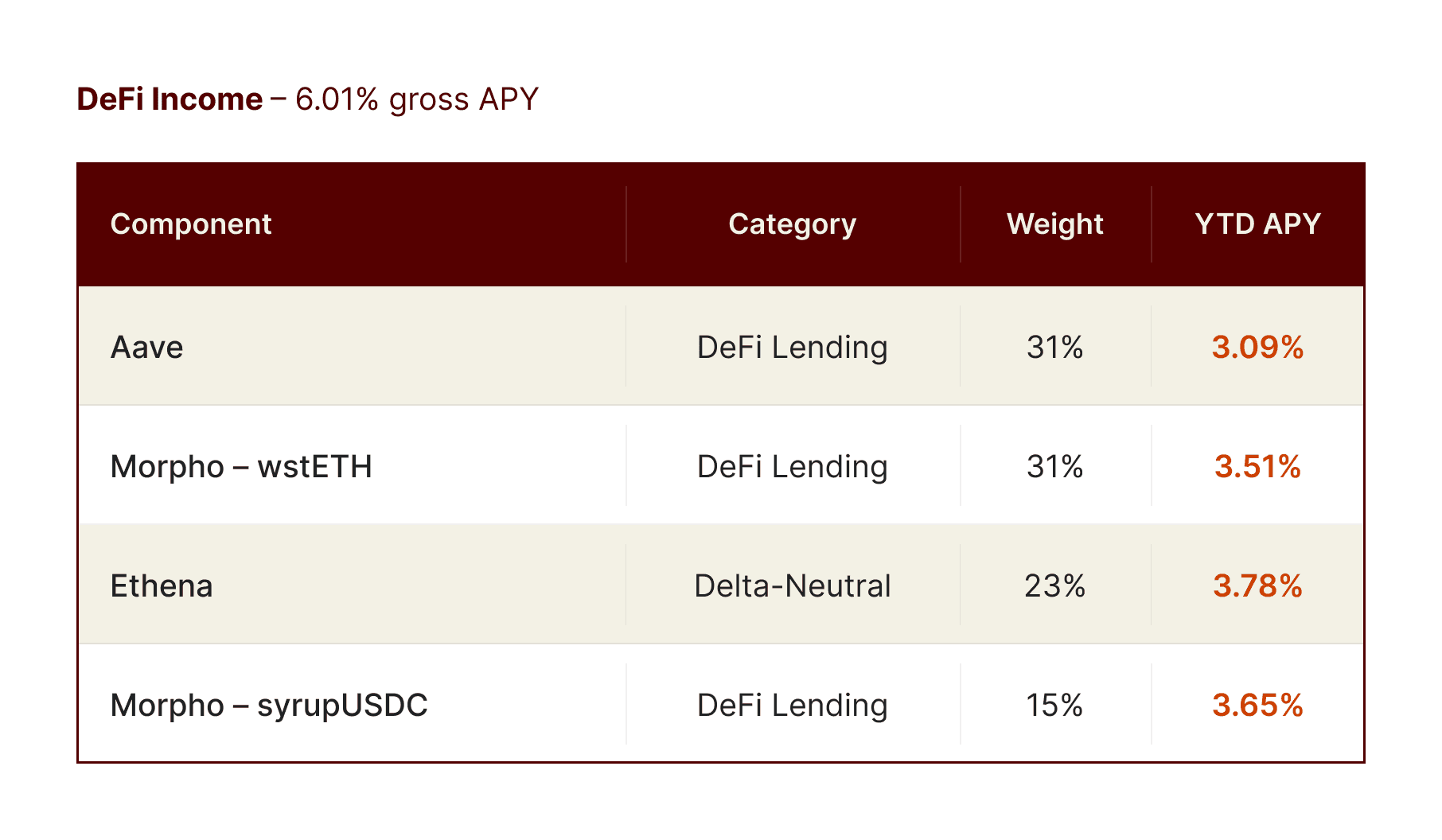

Breaking the correlation

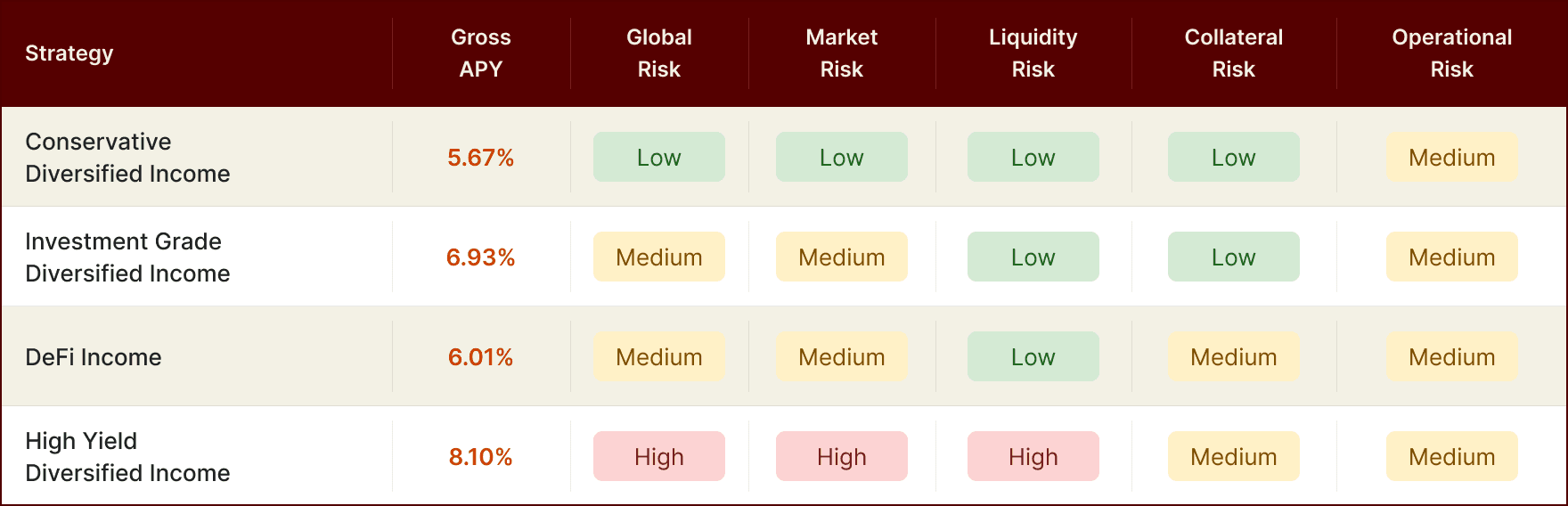

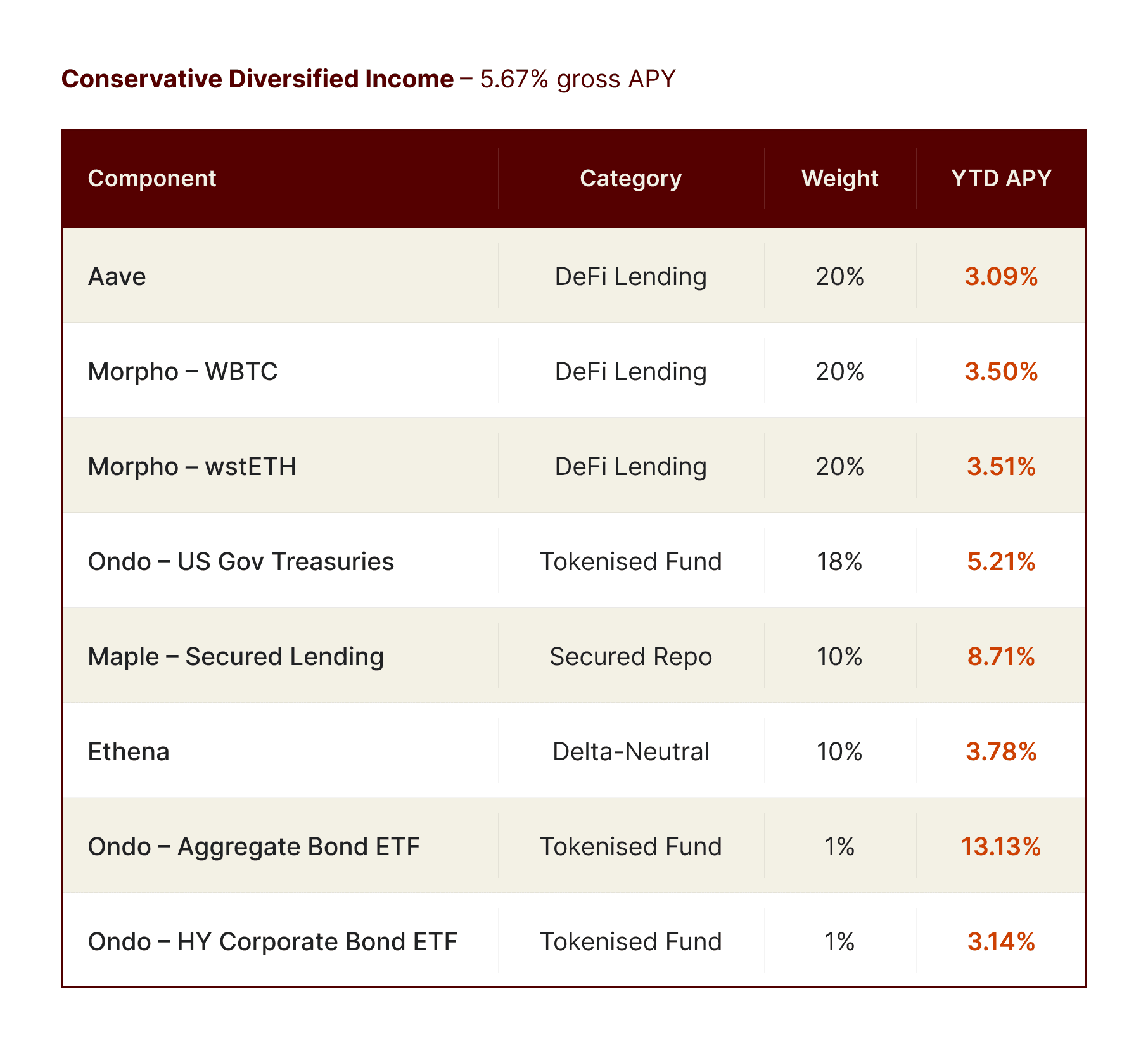

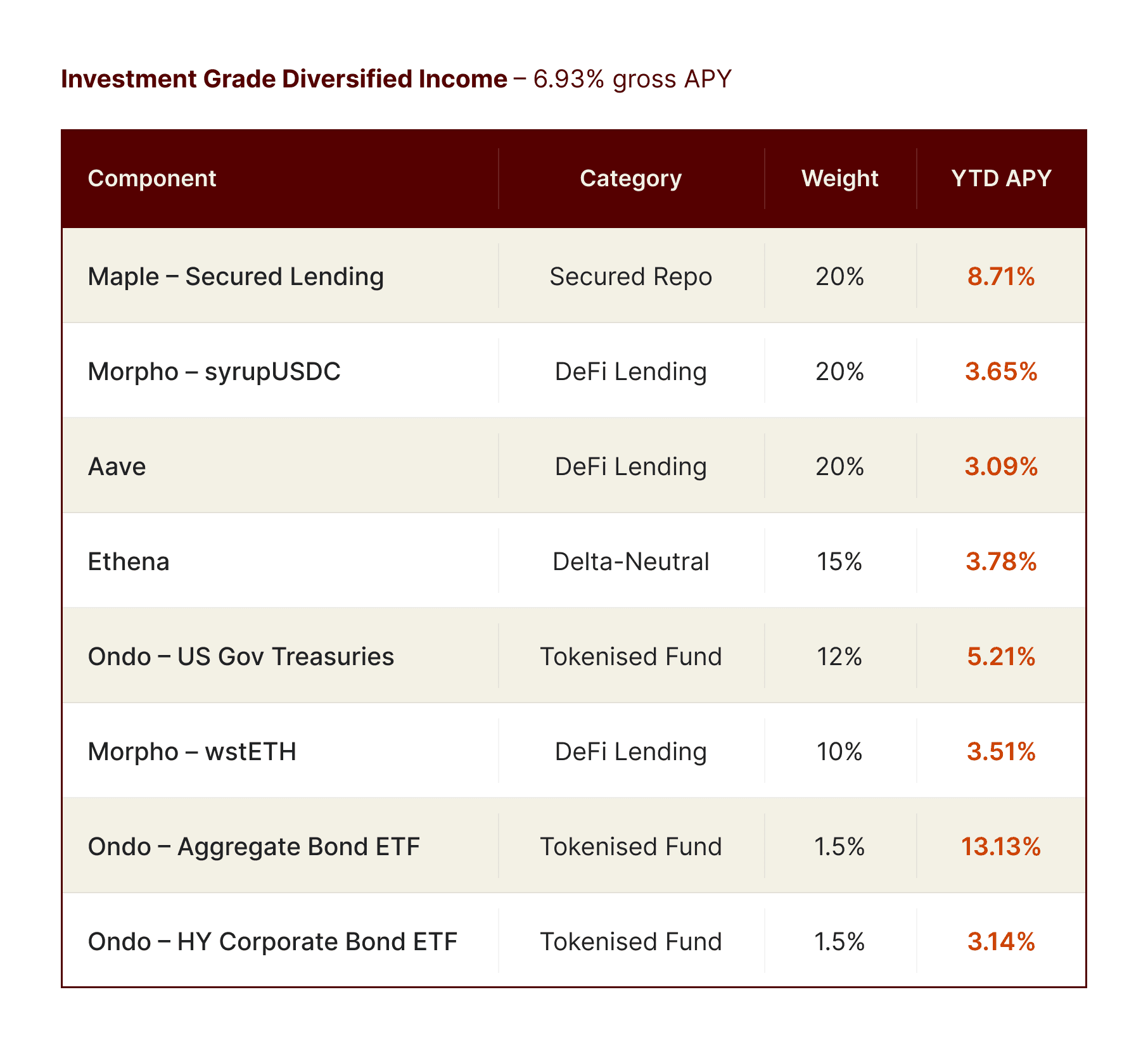

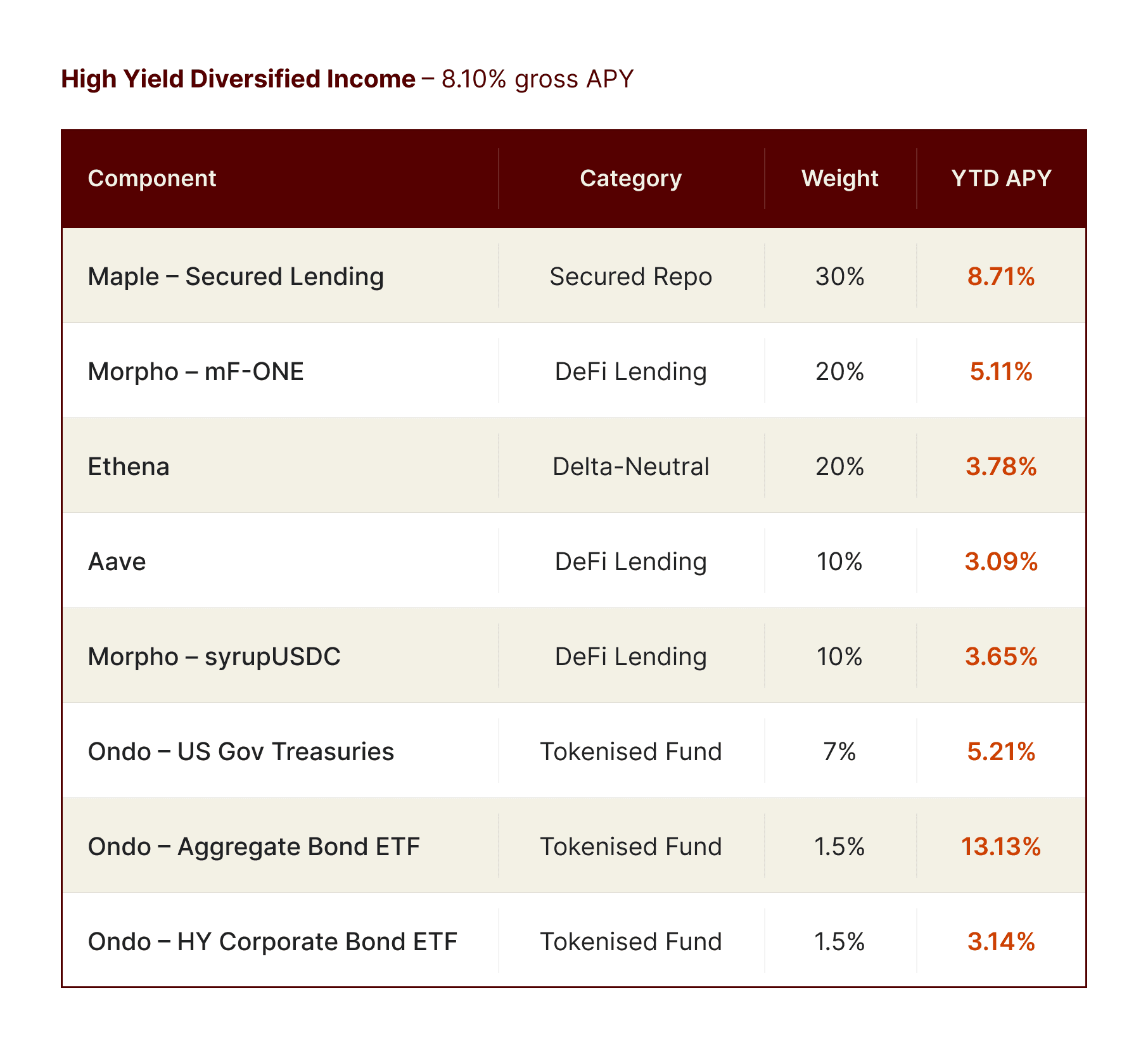

CoinShares introduced a different approach. Their suite spans four USDC-denominated strategies on Ethereum – all with 24/7 liquidity, weekly rebalancing, no leverage, and no recursive lending:

End-of-month allocations as of Q1 2026:

What separates these from most onchain strategies is immediately visible in the table. Tokenised treasuries and bond ETFs are governed by macro interest rates and credit spreads – forces that have limited relationship to DeFi utilisation cycles. Maple's secured repos (8.71% YTD APY) provide collateral-backed lending with counterparty assessment. And Ethena's delta-neutral strategies capture funding rate differentials in perpetual futures markets, driven by speculative positioning and leverage demand.

The High Yield strategy illustrates the effect. Monthly returns ranged from 0.37% to 0.84% with an 8.10% gross APY – a wider band than the pure DeFi strategy, but with a higher floor. As DeFi lending rates compress, the non-lending allocations hold value.

The operational reality underneath

DeFi lending settles instantly – deposit, withdraw, compound, all within a single block. Tokenised treasuries carry T+1 settlement windows, redemption cutoffs, and KYC gates inherited from the underlying traditional instruments. Secured repos involve counterparty agreements, collateral monitoring, and credit assessment workflows. Basis strategies require coordinated position management across spot and derivatives markets.

A strategy that blends all four is combining different execution environments with different timing, different settlement assumptions, and different risk parameters – inside a single portfolio with unified NAV and 24/7 liquidity.

Existing onchain infrastructure wasn't built for this. Vault standards were designed for synchronous, single-protocol interactions. ERC-4626 assumes deposits and withdrawals happen atomically. ERC-7540 introduced asynchronous flows but wasn't architected for mixed synchronous and asynchronous assets within the same vehicle, or for partial fills, or for structured metadata tracking off-chain lifecycle events.

CoinShares manages this through weekly rebalancing, no leverage, and no recursive lending – constraints that simplify the operational problem considerably. But the constraints themselves suggest that the infrastructure to run these strategies at full complexity doesn't yet exist as a standard.

The missing risk layer

The first gap is execution infrastructure, the second – risk visibility.

CoinShares assigns granular risk ratings across each strategy – global, market, liquidity, collateral, and operational – rather than a single composite score. The Conservative strategy carries low risk across almost every dimension. The High Yield strategy carries high market and liquidity risk but only medium collateral and operational risk.

This decomposition is routine in traditional asset management. It's nearly absent in onchain yield. Most vault curators provide an APY figure and a strategy description. How different exposures interact under stress, where correlations emerge, which risk factors dominate in a drawdown – that analysis is left to the allocator, if it's done at all.

For allocators, this is a deployment barrier. Real-time visibility into exposure by asset type, protocol, collateral quality, and liquidity profile changes how positions are sized – compared to working from a yield figure and a vault description.

Where the data points

CoinShares' strategies are a useful signal for the direction of onchain yield. As more regulated asset managers enter the space, strategies will increasingly blend DeFi lending with tokenised fixed income, secured credit, and relative-value trades – the same multi-asset approach that defines income portfolios in traditional markets.

The strategies are already outgrowing the standards built to support them. Those dozens of vaults allocating the same pools aren't going away – but the distance between what they offer and what differentiated, multi-asset strategies require is becoming harder to ignore.

CoinShares' onchain yield strategies are managed by CoinShares Asset Management, authorised and regulated by the AMF under AIFMD, MiFID II, and MiCA. All performance figures cited are gross, backtested over Jan 2025 to Feb 2026, and not indicative of future results. Capital is at risk. This article is for informational purposes only and does not constitute investment advice.